Running a small business right now feels like trying to juggle while someone keeps throwing more balls at you. Inflation’s still crazy. Customers pay slower than molasses. Banks act like lending money is doing you a personal favor.

I’ve watched businesses with great products go under because they couldn’t manage their cash. Managing small business finances in 2025 isn’t just about having a good accountant anymore. You need street-smart strategies that actually work when money gets tight.

Here’s what I’ve learned helping small businesses stay alive and kicking over the past eight years.

Cash Flow Reality Check

Check Your Cash Every Single Day

Look, I get it. Checking your bank balance daily feels obsessive. But you know what’s worse? Bouncing a check to your biggest supplier because you thought you had more money than you actually did.

My buddy runs a small landscaping company. Used to check his balance maybe twice a week. Then he started tracking daily and realized his pattern – Mondays were always brutal because weekend sales took days to hit his account, but his crew needed to be paid right away.

Simple fix once he saw it. Now he knows to keep extra cash available on Mondays.

Get a simple spreadsheet or use whatever software you like. Just track what’s coming in today, what’s going out today, and what you’ll have left. Do this every morning with your coffee.

Get Your Money Faster

The biggest mistake most small businesses make? They’re way too nice about collecting money.

Send invoices the minute work is done. Not next week when you get around to it. The second you finish a job, that invoice should go out.

Offer discounts for fast payment. Tell customers they get 2% off if they pay within 10 days. Trust me, getting 98% of your money in 10 days beats getting 100% in 45 days. Your cash flow will thank you.

Accept credit cards, PayPal, Venmo, whatever makes it easier for people to pay you quickly. Every day you wait for a check to clear is money you can’t use for your business.

Call people when they’re late. I know it’s awkward, but so is going out of business because people owe you money. Be polite but firm.

Pay Your Bills Smarter

This doesn’t mean stiffing your vendors. It means being strategic about when you pay.

If someone gives you 30 days to pay, use all 30 days. Your money can sit in your account earning interest (even if it’s tiny) instead of theirs.

Ask your regular suppliers for longer payment terms. The worst they can say is no, but many will give good customers 45 or even 60 days if you’ve been paying on time.

Use credit cards for big purchases when you can. Gives you another month before you actually have to pay. Just make sure you can pay the full balance when it’s due.

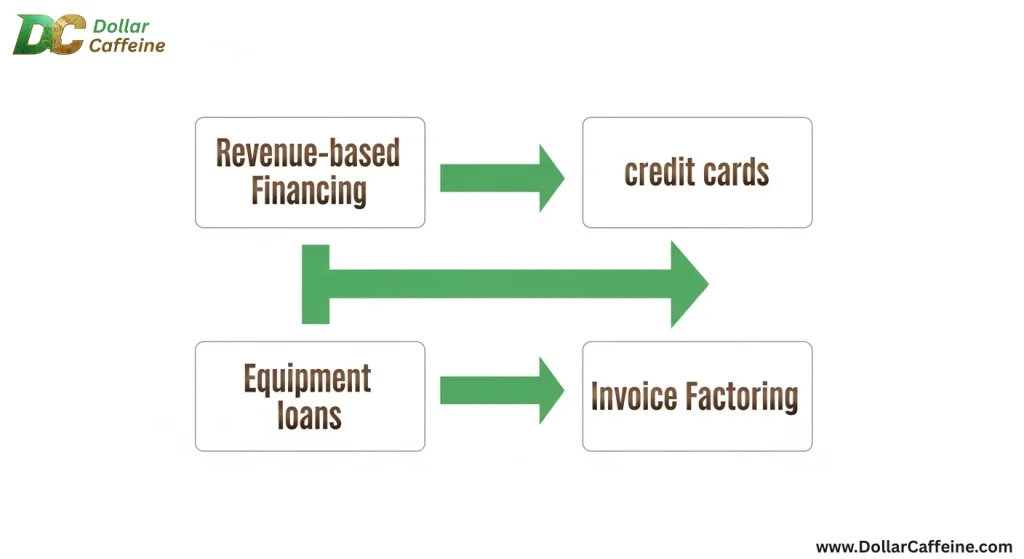

Finding Money When You Need It

Revenue-Based Financing

This is becoming huge because traditional bank loans are such a pain right now. Here’s how it works – you get cash up front, then pay back a percentage of your monthly sales until you’ve paid back about 1.2 to 1.5 times what you borrowed.

So if you borrow $50,000, you might pay 8% of your monthly revenue until you’ve paid back $60,000 total.

The cool thing? If you have a bad month, your payment is lower. If you have a great month, you pay more but get done faster.

Companies like Clearco do this stuff. It’s more expensive than a bank loan, but way faster and easier to get.

Business Credit Cards (Yeah, Really)

Everyone says don’t use credit cards for business. Sometimes everyone is wrong.

Get a few business cards with different billing cycles. Spread your purchases across them to maximize the time before you have to pay.

Look for 0% intro rates. Some cards give you 12-18 months with no interest. Perfect for buying equipment or stocking up on inventory.

Use the cash back. 2% back on everything adds up fast. One client of mine makes an extra $800 a month just from credit card rewards.

Just don’t be stupid about it. Have a plan for paying them off.

Equipment Financing

Need a new truck or equipment but don’t want to blow all your cash? Equipment loans are usually easier to get because the equipment itself is collateral.

You can usually get 3-7 year terms, which keeps your monthly payments reasonable. And here’s the kicker – sometimes it makes sense to finance even if you have the cash, because you keep your working capital available for day-to-day operations.

Invoice Factoring

Got customers who owe you money but you need cash now? Factoring companies will buy your invoices and give you cash immediately.

You get about 80-90% of what you’re owed right away. They collect from your customer, then give you the rest minus their fee.

It’s not cheap – usually costs 1-5% of the invoice value per month. But if you’re in a cash crunch, it can save your bacon.

Smart Money Management

Keep Some Cash for Emergencies

Every business needs a rainy day fund. Start small – even $5,000 is better than nothing. Work toward having at least one month of expenses saved up.

Keep it somewhere safe but accessible. A high-yield savings account or money market fund works fine. Don’t try to invest it or get fancy. You need to be able to get to it quickly when something goes wrong.

How do you build it? Set aside 2-5% of every dollar that comes in until you hit your target. Make it automatic so you don’t accidentally spend it.

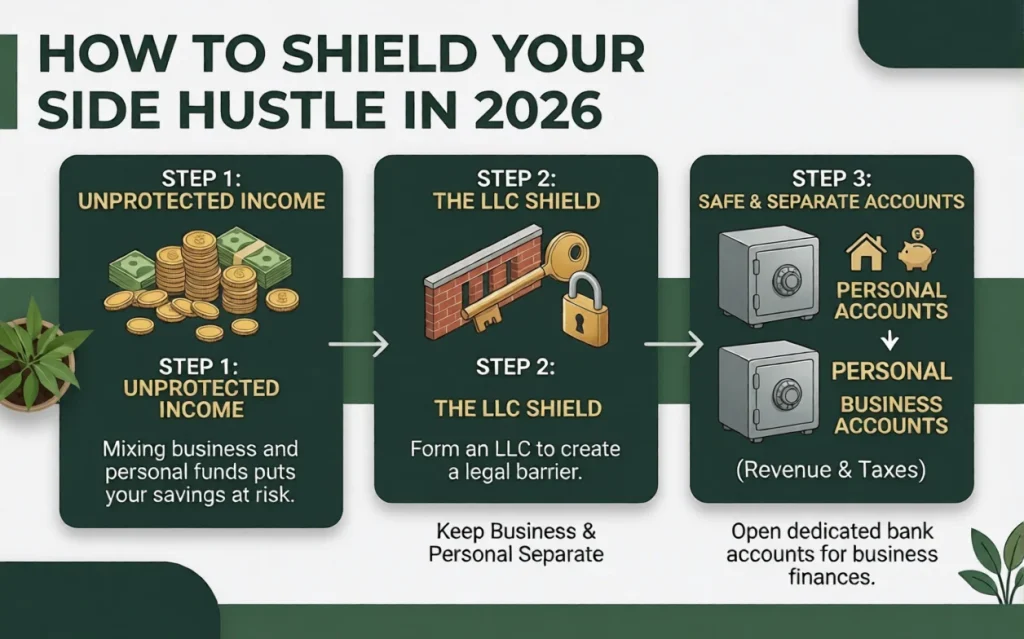

Keep Business and Personal Money Separate

This seems obvious but you’d be amazed how many people screw this up. Mixing business and personal money makes everything harder – taxes, legal protection, figuring out how your business is actually doing.

Get a business checking account even if you’re just freelancing. Get a business credit card. Pay yourself a regular amount from the business to your personal account instead of just grabbing money whenever you need it.

Use Software That Doesn’t Suck

QuickBooks, Xero, FreshBooks – pick one and actually use it. Trying to track everything with spreadsheets or (God help you) paper receipts in 2025 is like trying to compete in NASCAR with a horse and buggy.

Connect your bank accounts so transactions import automatically. Review everything weekly to make sure it’s categorized right. This stuff pays for itself by saving you time and preventing mistakes.

Watch The Numbers That Matter

You don’t need to be a finance genius, but you need to track some basic stuff:

How long does it take customers to pay you? If it’s getting longer, that’s a problem.

What’s your gross profit on each sale? If this number is going down, you’re in trouble even if sales are going up.

How much cash do you have compared to what you owe short-term? This tells you if you can pay your bills next month.

Funding Options That Work

SBA Loans (If You Have Time)

Small Business Administration loans have great rates and terms, but they take forever and require tons of paperwork. Good option if you’re planning ahead and have decent credit.

Online Lenders

Faster than banks but more expensive. Companies like OnDeck or Kabbage can get you money in days instead of months. Just make sure you can handle the payments – they’re usually daily or weekly.

Friends and Family

Borrowing from people you know can be the cheapest money you’ll find. Just make sure you treat it like a real business loan with written terms. Nothing ruins relationships faster than unclear money agreements.

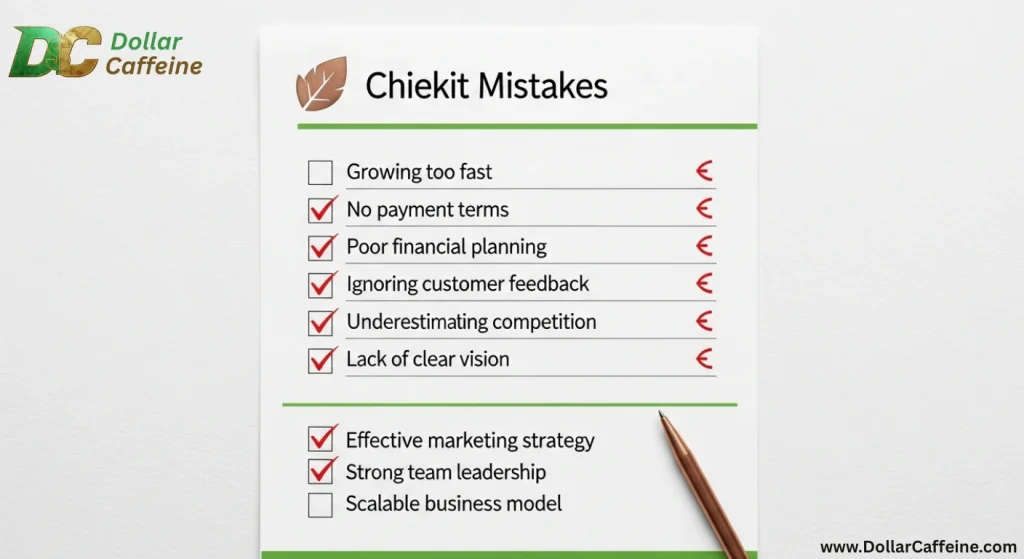

Mistakes That Kill Businesses

Growing too fast. More sales sound great until you realize you don’t have the cash to fulfill all those orders. Every new customer ties up working capital.

Not having payment terms. Tell customers exactly when payment is due, or they’ll pay you whenever they remember. Which might be never.

Chasing sales numbers while ignoring profit. Look, big revenue sounds impressive at parties, but profit is what keeps the lights on. You can’t pay rent with bragging rights.

Waiting until you’re broke to find money. Banks have this weird ability to detect desperation from three states away. Build relationships with lenders when you don’t need anything from them.

People Also Ask

How much emergency cash do I actually need?

Whatever you can scrape together to start – even a thousand bucks is better than zero. Eventually you want enough to cover a month of bills, but don’t stress if you can’t get there overnight. Depends on whether your income is steady or all over the place.

What’s the quickest way to get funding when I need it?

Business credit cards or revenue-based loans. Bank loans? Forget it unless you’ve got months to wait and perfect paperwork. Online lenders move faster but they’ll cost you more.

Do I really need QuickBooks or can I just use Excel?

Excel’s fine if you’re basically a one-person show. But once you have people working for you or inventory to track, get real accounting software. Your sanity will thank you.

How do I know if my business money situation is okay?

Simple test: Can you pay everything on time? Got some money sitting around for surprises? Are you still making decent profit on what you sell? If yes to all three, you’re doing better than most.

Real Business Owner Experiences

The Small Business Administration says 82% of business failures come from cash flow problems, not lack of customers or bad products. Source: SBA Statistics

JP Morgan’s research shows most small businesses only have about 27 days of cash on hand. That’s not much buffer when things go wrong. Source: JP Morgan Institute

A survey by the National Federation of Independent Business found that getting credit is now the biggest concern for 23% of small business owners. Source: NFIB Report

Data from Kabbage shows businesses that track their cash flow daily are three times more likely to survive economic downturns. Source: Kabbage Study

What to Do Right Now

This week, start tracking your cash daily. Just a simple spreadsheet showing what came in, what went out, and what’s left.

Call or email everyone who owes you money. Be nice but firm about when you expect payment.

No business credit card yet? Get one this week. Seriously. Even if it sits in your wallet collecting dust, you’ll be glad it’s there when your main client pays late and payroll is due.

Next month, get some real accounting software if you’re still using spreadsheets. QuickBooks isn’t perfect, but it beats the heck out of shoebox bookkeeping. And hey, start throwing money into that emergency fund – even fifty bucks a week adds up.

Don’t wait until you’re desperate to research funding. Talk to lenders now while you don’t need anything. They’re way nicer when you’re not begging for money to make payroll.

The Real Deal

Managing small business finances in 2025 isn’t complicated, but it’s not optional either. Track your cash, collect money faster, and always have a backup plan.

Skip the expensive consultants and fancy MBA strategies. What you need is pretty basic – systems that show you where your money is and the guts to actually use them every day.

The businesses surviving right now? They’re not always the ones with the coolest products or biggest marketing budgets. They’re the ones who know exactly how much money they have and where it’s going.

Don’t try to do everything at once. Pick two things from this guide and actually do them this week. Your future stressed-out self will send you a thank-you card. Your bank account will thank you.

Read more blog about finance on DollarCaffeine .