Paying off debt sucks. I know because I’ve been there.

You send money every month to credit cards and loans. But somehow the balances stay almost the same. It’s frustrating as hell.

The good news? There are two methods that actually work. The debt snowball vs. debt avalanche debate has helped millions of people get out of debt. But which one should you pick?

I’ll break down both methods for you. Real examples. Pros and cons. Expert opinions. By the end, you’ll know exactly which plan fits your situation.

Let’s get started.

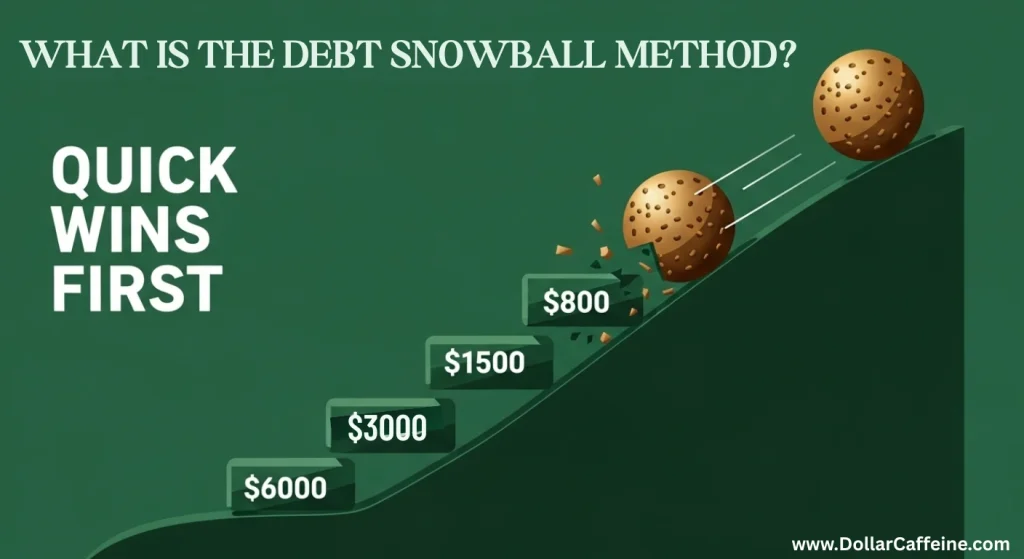

What is the Debt Snowball Method?

Dave Ramsey made this method famous. It’s pretty simple actually.

You pay off your smallest debt first. Not the one with the highest interest rate. Just the smallest balance.

Here’s how it works:

Write down all your debts. Put them in order from smallest to largest balance. Pay the minimum on everything. Then throw every extra dollar at that tiny debt.

When it’s gone, you take that payment and add it to the next debt. It’s like a snowball rolling downhill. Gets bigger and bigger.

Example of Debt Snowball

Let’s say you have these debts:

- Credit card: $800 (19% interest)

- Medical bill: $1,500 (no interest)

- Car loan: $6,000 (7% interest)

- Student loan: $12,000 (5% interest)

With snowball, you attack the $800 credit card first. Even though the medical bill has no interest, you ignore it for now.

Why does this work? Because you get a win fast. That $800 disappears in a few months. You feel good. You stay motivated.

The Psychology Behind It

Northwestern University did a study on this. They found something interesting. People who paid small debts first were way more likely to pay off everything.

It’s not about math. It’s about your brain. When you eliminate a debt, you get a hit of dopamine. That’s your reward chemical. It makes you want to keep going.

Dr. Blake McShane led the study. He said behavior beats math when it comes to debt payoff. Makes sense to me.

What is the Debt Avalanche Method?

This method is all about the numbers. You go after the highest interest rate first.

It’s more logical than snowball. But also harder to stick with sometimes.

Here’s the process:

List your debts by interest rate. Highest to lowest. Pay minimums on everything. Put more money on the debt with the worst interest rate.

When that’s gone, move to the next highest rate. Keep going until you’re debt free.

Example of Debt Avalanche

Same debts as before:

- Credit card: $800 (19% interest) ← Start here

- Car loan: $6,000 (7% interest)

- Student loan: $12,000 (5% interest)

- Medical bill: $1,500 (no interest) ← Do this last

You’d still hit the credit card first. But then you’d tackle the car loan instead of the medical bill. Because 7% costs more than 0%.

Why Avalanche Saves Money

Simple math here. High interest rates means you have to pay more money over time. When you eliminate them first, you save the most cash.

Financial experts love this method. It usually gets you out of debt faster and cheaper than snowball.

Debt Snowball vs. Debt Avalanche: Comprehensive Comparison

| Factor | Debt Snowball | Debt Avalanche |

| Primary Focus | Smallest balance first | Highest interest rate first |

| Motivation Level | High (quick wins) | Moderate (slower start) |

| Total Cost | Usually higher | Typically lower |

| Time to Freedom | Often longer | Generally shorter |

| Best Personality Type | Needs encouragement | Self-disciplined |

| Complexity | Very simple | Slightly more complex |

| Success Rate | Higher adherence | Lower adherence |

Pros and Cons Breakdown

Debt Snowball Pros

You see progress fast. That first debt might disappear in 2-3 months. Feels amazing.

It’s super simple. No calculations needed. Just pay the smallest one first.

You’re more likely to stick with it. Studies prove this. Quick wins keep you going.

Builds confidence. Each debt you kill makes you feel stronger.

Debt Snowball Cons

Costs more money overall. Those high interest rates keep charging you.

Takes longer to get debt free. Could be months or years longer.

Not the smartest math. You’re ignoring expensive debt to pay cheap debt.

Debt Avalanche Pros

Saves the most money. You pay less interest overall.

Gets you debt free faster in most cases. Math doesn’t lie.

Makes logical sense. Attack the most expensive debt first.

Debt Avalanche Cons

Takes forever to see the first debt disappear. Can be discouraging.

Requires discipline. You need willpower when progress feels slow.

Some people quit before they see results.

Real Example: Sarah’s Debt Journey

Sarah is a teacher. She’s 32 and has these debts:

- Credit card #1: $2,800 at 21%

- Credit card #2: $4,200 at 16%

- Car loan: $9,500 at 8%

- Student loans: $15,000 at 6%

Total debt: $31,500. She can pay an extra $400 per month.

If Sarah Uses Snowball:

She pays off credit card #1 first ($2,800). Takes about 8 months.

Then credit card #2. Then the car. Finally student loans.

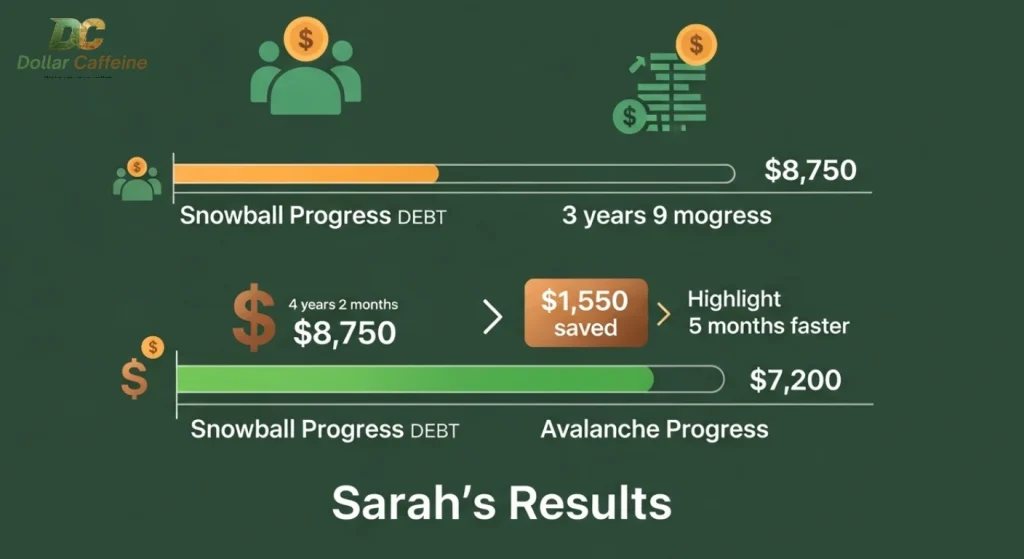

Total time: 4 years, 2 months Total interest paid: $8,750

If Sarah Uses Avalanche:

Same first target – credit card #1 has the highest rate (21%).

Then credit card #2 (16%). Then car (8%). Finally student loans (6%).

Total time: 3 years, 9 months

Total interest paid: $7,200

Sarah saves $1,550 and 5 months with avalanche. But both methods start with the same debt, so she’d feel motivated either way.

What Experts Say

Dave Ramsey’s Take

Dave is all about snowball. He’s helped millions of people get out of debt with this method.

His company says people using snowball are 70% more likely to pay off all their debts. That’s a big difference.

He argues that debt is behavioral, not mathematical. I tend to agree with him on this.

Source: Dave Ramsey Solutions – Debt Snowball Method

NerdWallet’s Opinion

They recommend avalanche for most people. Their calculators show you save about $1,847 on average.

They have a point. Math is math. Higher interest rates cost more money.

But they also admit snowball works better for some personalities.

Source: NerdWallet Debt Avalanche Guide

What Harvard Found

Harvard Business School studied 50,000 people trying to pay off debt. Their finding was interesting.

The method matters less than consistency. People who stuck with any plan did way better than people who kept switching strategies.

They also found debt consolidation helped both methods work better.

Source: Harvard Business Review – Debt Repayment Psychology

Reddit Users Weigh In

The personal finance community on Reddit has a simple message. Use whichever method you won’t quit.

Most successful stories involve people who picked one method and stuck with it for years.

The failures usually involve people who kept switching between methods.

Source: Reddit Personal Finance Wiki

People Also Ask

Which method pays off debt faster?

Avalanche usually wins on speed. You save months or even years compared to snowball.

But only if you actually stick with it. Snowball might be faster for you if avalanche makes you quit.

Can I mix both methods?

Sure. Some people start with snowball to get motivated. Once they knock out 2-3 small debts, they switch to avalanche.

This hybrid approach gives you early wins plus long-term savings.

What if I have mostly credit card debt?

Avalanche is probably better. Credit cards usually have the highest interest rates.

But if you have several small cards under $1,000, snowball might keep you motivated.

Does snowball really work for big debts?

It works, but takes longer and costs more. The key is staying consistent for years.

If you’ve failed before with other methods, snowball might be your best shot.

What about debt consolidation?

Consolidation can help either method. You combine multiple debts into one payment.

If you get a lower interest rate, even better. Then you can use snowball or avalanche on the consolidated debt.

Should I pay minimums on everything else?

Yes, always. Late fees and penalties will mess up any debt payoff plan.

Set up autopay for minimums. Then manually add extra to your target debt.

Advanced Tips That Actually Work

Find Extra Money

Look for cash you can throw at debt:

Sell stuff you don’t use. Facebook Marketplace and eBay work great.

Pick up a side job. Even $200 extra per month makes a huge difference.

Use tax refunds. Don’t blow it on vacation. Kill a debt instead.

Cut one big expense temporarily. Cancel cable or eat out less.

Make It Automatic

Set up autopay for all minimum payments. This prevents late fees when you’re busy.

Automate extra payments too if possible. Makes it harder to spend that money elsewhere.

Track Your Progress

Use an app or spreadsheet. Watching balances drop is motivating.

Some people make charts on their wall. Visual progress feels good.

Negotiate with Companies

Call your credit card companies. Ask for lower interest rates.

Many will reduce rates if you ask nicely. Especially if you’ve been paying on time.

Don’t Create New Debt

Hide your credit cards. Delete shopping apps from your phone.

Make it physically hard to spend money you don’t have.

Which Method Should You Choose?

Pick Debt Snowball If:

You need to see progress fast. Waiting a year for the first payoff will discourage you.

You’ve tried to pay off debt before and quit. Snowball gives you more wins to celebrate.

You have several small debts under $2,000. These disappear quickly with snowball.

Motivation matters more to you than saving money.

Pick Debt Avalanche If:

You’re disciplined and patient. You can handle slow progress at first.

You want to save as much money as possible. Math matters more than feelings.

Most of your debt is high-interest credit cards. Avalanche shines here.

You successfully completed other long-term goals before.

Try a Hybrid Approach If:

You want the best of both worlds. Start with snowball for motivation, then switch to avalanche.

You have a mix of small and large debts. Use snowball for small ones, avalanche for big ones.

Your Action Plan

This Week

List all your debts. Include balances and interest rates.

Calculate how much extra you can pay each month.

Choose snowball or avalanche based on your personality.

Set up autopay for all minimum payments.

Next Month

Start attacking your first target debt with extra payments.

Track your progress weekly.

Celebrate when you make the first debt disappear.

Keep Going

Don’t switch methods unless you’re really struggling.

Find more money to throw at debt when possible.

Stay connected with supportive friends or online communities.

Final Thoughts

The debt snowball vs. debt avalanche debate will continue forever. Both methods work.

Snowball gives you psychological wins. Avalanche gives you mathematical wins.

The truth is simple: pick the method you’ll actually follow. Consistency beats perfection every time.

I’ve seen people succeed with both approaches. I’ve also seen people fail with both. The difference wasn’t the method. It was their commitment.

Whatever you choose, start today. Not next month. Not after the holidays. Today.

Your future debt-free self is counting on you.

Read more about finance on DollarCafeine