Okay, let’s be real. You’ve probably downloaded like five different budgeting apps, used them for a week, then gave up.

I get it. Most apps are either too complicated, too simple, or just plain annoying.

I’ve spent the last six months testing every best budgeting apps for Americans I could find. Some were amazing. Some made me want to throw my phone.

Here’s what actually works in 2025.

The Best Free Budgeting Apps

1. Mint – Still the King (But Getting Old)

Mint has been around forever. There’s a reason it’s still popular.

What’s good:

- Connects to basically every American bank

- Automatically categorizes your spending

- Shows your credit score for free

- Bill reminders that actually work

- Zero cost, ever

What sucks:

- The interface looks like it’s from 2015

- Sometimes takes days to sync transactions

- Ads everywhere

- Customer service is terrible

Who should use it: People who want automatic tracking without thinking about it.

I’ve used Mint on and off for three years. It’s not sexy, but it works. If you just want to see where your money goes without much effort, it’s solid.

2. Personal Capital – Great for the Big Picture

Personal Capital is weird because it’s half budgeting app, half investment tracker.

What’s good:

- Amazing dashboard showing all your accounts

- Net worth tracking that’s actually motivating

- Investment fee analyzer (this saved me $200/year)

- Works with 401k accounts

- Free financial advisors (if you have $100k+)

What sucks:

- Not great for day-to-day budgeting

- Pushes investment services hard

- Can be overwhelming if you’re just starting

Who should use it: People who want to see their complete financial picture.

I love Personal Capital for seeing everything in one place. But if you’re broke and just trying to budget groceries, it’s overkill.

3. Goodbudget – Envelope Method Made Digital

Remember when your grandma used envelopes for budgeting? This app does that digitally.

What’s good:

- Perfect if you overspend in certain categories

- Envelope method actually works for stopping overspending

- Syncs between partners/spouses

- Simple and clean design

- Free version handles 10 envelopes

What sucks:

- Doesn’t connect to bank accounts automatically

- You have to manually enter everything

- Limited envelopes on free plan

- Can feel restrictive

Who should use it: People who need strict spending controls.

This app saved my friend Sarah from overspending on dining out. She puts $200 in her “restaurants” envelope each month. When it’s gone, she cooks at home.

The Best Premium Apps (Worth Paying For)

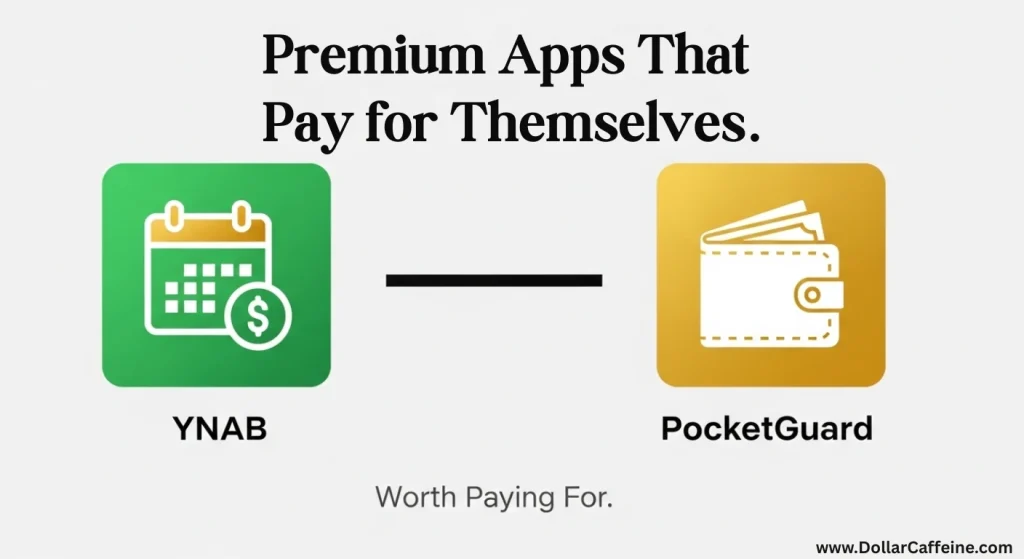

4. YNAB (You Need A Budget) – The Gold Standard

YNAB costs $99/year, but it’s the best budgeting app I’ve ever used.

What’s good:

- Forces you to give every dollar a job

- Incredible customer support

- Free classes that actually teach you budgeting

- Syncs with American banks perfectly

- Mobile app is fantastic

- 34-day free trial

What sucks:

- Costs money (duh)

- Learning curve is steep

- Can be overwhelming at first

- Philosophy is intense

Who should use it: People serious about changing their money habits.

YNAB users save an average of $600 in their first two months. That pays for six years of the app.

I used YNAB for a year and it completely changed how I think about money. But it’s not casual. You have to commit.

5. PocketGuard – Simple Spending Tracker

PocketGuard has one job: tell you how much you can safely spend.

What’s good:

- Shows “In My Pocket” amount after bills and savings

- Prevents overspending automatically

- Simple interface anyone can understand

- Finds subscriptions you forgot about

- Negotiates bills for you (premium feature)

What sucks:

- Premium features cost $12.99/month

- Limited customization

- Sometimes too simple

- Bill negotiation doesn’t always work

Who should use it: People who just want to know if they can afford something.

My sister uses PocketGuard because she hated complicated budgets. She just wants to know: “Can I buy this or not?”

Apps That Work Great on iPhone and Android

6. Simplifi by Quicken – New Kid on the Block

Quicken launched this in 2020 and it’s really solid.

What’s good:

- Beautiful, modern design

- Excellent mobile app

- Great customer support

- Customizable categories

- Syncs across all devices perfectly

- $3.99/month isn’t bad

What sucks:

- No free version

- Still building features

- Not many integrations yet

- Limited investment tracking

Who should use it: People who want modern design and don’t mind paying.

Simplifi feels like what Mint should have become. Clean, fast, and actually enjoyable to use.

7. Tiller – Spreadsheets but Better

Tiller connects your bank accounts to Google Sheets or Excel.

What’s good:

- Ultimate customization

- Uses spreadsheets you already know

- Automatic transaction import

- Great for couples who want to customize everything

- 30-day free trial, then $79/year

What sucks:

- You need to know spreadsheets

- Takes time to set up properly

- Not good for beginners

- Can become overwhelming

Who should use it: Spreadsheet nerds who want bank connectivity.

If you love Excel and want total control, Tiller is amazing. If spreadsheets scare you, skip it.

Best Apps for Specific Situations

8. Honeydue – Built for Couples

Managing money as a couple is hard. Honeydue makes it easier.

What’s good:

- Both partners can see everything

- Set up shared and individual budgets

- Chat about transactions in the app

- Bill reminders for both people

- Free to use

What sucks:

- Limited features for single people

- Sometimes syncing issues

- Interface could be better

- Not great for complex finances

Who should use it: Couples who want to budget together.

My friends Jake and Maria use this to avoid money fights. They can both see spending without having to ask questions.

9. Spendee – Pretty but Functional

Spendee focuses on making budgeting visually appealing.

What’s good:

- Gorgeous interface with custom categories

- Great for visual learners

- Excellent spending analytics

- Multiple wallet support

- Works worldwide

What sucks:

- Premium features cost extra

- Can be more style than substance

- Limited American bank connections

- Learning curve for features

Who should use it: People who need pretty apps to stay motivated.

If boring apps make you quit budgeting, Spendee might keep you engaged.

10. Zeta – Another Couples App

Zeta is like Honeydue but with more features.

What’s good:

- Joint and individual account tracking

- Shared goals and budgets

- Bill splitting made easy

- Good customer support

- Free basic version

What sucks:

- Premium costs $9/month

- Still building user base

- Limited bank connections

- Can be slow sometimes

Who should use it: Couples who want more features than Honeydue.

Specialty Apps Worth Knowing About

11. EveryDollar – Dave Ramsey’s App

If you follow Dave Ramsey, this is his official budgeting app.

What’s good:

- Zero-based budgeting approach

- Follows Baby Steps method

- Simple interface

- Free version available

- Good for debt payoff

What sucks:

- Very basic unless you pay

- Dave Ramsey’s advice isn’t for everyone

- Limited features

- $129/year for bank connection

Who should use it: Dave Ramsey followers or zero-based budget fans.

12. Albert – AI-Powered Money Coach

Albert uses artificial intelligence to help you save and budget.

What’s good:

- Automatic savings based on spending patterns

- AI gives personalized money tips

- No overdraft fees

- Genius feature gives advice

- Modern, clean design

What sucks:

- Monthly fee for most features

- Limited budgeting tools

- More focused on saving than budgeting

- Still learning your habits

Who should use it: People who want automated money management.

Micro-Investment Apps That Include Budgeting

13. Acorns – Invest Your Spare Change

Acorns rounds up purchases and invests the change.

What’s good:

- Automatic investing is effortless

- Good for beginners

- Basic budgeting features

- Educational content

- $1-3/month pricing tiers

What sucks:

- Fees can eat small accounts

- Limited budgeting features

- Investment options are basic

- Better for investing than budgeting

Who should use it: People who want to start investing while budgeting.

14. Stash – Budgeting Plus Investing

Stash combines budgeting with beginner investing.

What’s good:

- Start investing with $5

- Educational approach to money

- Banking features included

- Goal-based saving

- $1-9/month pricing

What sucks:

- Monthly fees add up

- Limited budgeting compared to dedicated apps

- Investment options are limited

- Can be overwhelming for pure budgeting

Who should use it: People ready to budget and invest simultaneously.

Banking Apps with Built-In Budgeting

15. Capital One Shopping and Eno

Your bank might have better budgeting tools than you think.

Capital One customers get:

- Automatic spending categories

- Bill tracking and alerts

- Credit monitoring

- Savings goal tracking

- All free with your account

Other banks with good tools:

- Chase offers spending breakdowns

- Bank of America has budgeting in their app

- Ally Bank has excellent savings tools

- Wells Fargo has spending insights

Who should check this: Everyone. Start with your bank’s app before downloading others.

Red Flags: Apps to Avoid

Some apps look good but have serious problems.

Avoid apps that:

- Charge surprise fees

- Don’t use bank-level security

- Have terrible reviews for customer service

- Promise unrealistic results

- Don’t clearly explain their business model

Specific apps I’d skip:

- Digit (too many fee complaints)

- Qapital (customer service issues)

- Various apps with under 100 reviews

Do your research. Read recent reviews. If something seems too good to be true, it probably is.

How to Choose the Right App for You

Ask yourself these questions:

What’s your main problem?

- Overspending = Envelope apps like Goodbudget

- No idea where money goes = Automatic trackers like Mint

- Want to change money habits = YNAB

- Just need spending limits = PocketGuard

How much time do you want to spend?

- 5 minutes a month = Mint or Personal Capital

- 30 minutes a week = YNAB or Simplifi

- Daily involvement = Envelope method apps

Are you budgeting alone or with someone?

- Solo = Any app works

- Couple = Honeydue, Zeta, or shared YNAB account

What’s your tech comfort level?

- Love technology = Tiller or advanced features

- Keep it simple = PocketGuard or basic Mint

- Middle ground = YNAB or Simplifi

Tips for Actually Sticking with Your App

Most people download an app, use it for two weeks, then forget about it.

How to make it stick:

Start with one thing. Don’t try to set up a perfect budget on day one. Just track spending for a week.

Set phone reminders. Most apps are worthless if you don’t open them regularly.

Connect your main accounts first. Don’t worry about that old savings account with $12 in it.

Use notifications wisely. Turn on spending alerts, turn off promotional messages.

Give it a real trial. Use any app for at least a month before deciding if it works.

Don’t app-hop. Switching apps every few weeks means you never learn any of them properly.

My Personal Recommendations

After testing everything, here’s what I’d recommend:

If you want free and automatic: Mint If you’re serious about changing habits: YNAB

If you want simple spending limits: PocketGuard If you’re budgeting as a couple: Honeydue If you love spreadsheets: Tiller If you want modern design: Simplifi

My personal setup: I use YNAB for budgeting and Personal Capital to see my net worth. That covers everything I need.

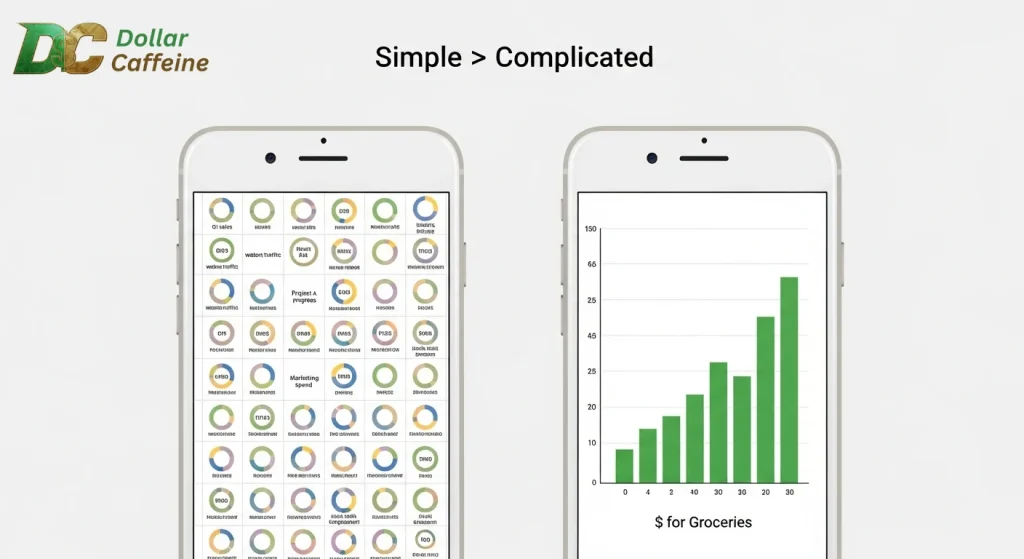

Why Most Budgeting Apps Fail

let’s talk about why you probably hate budgeting apps.

Most apps are built by tech people who’ve never struggled with money. They think everyone wants 47 different categories and pie charts for everything.

Real people just want to know:

Do I have enough money for groceries?

Can I afford to go out this weekend?

The best budgeting apps for Americans in 2025 get this. They make money management simple, not complicated.

Conclusion

The best budgeting apps for Americans in 2025 aren’t necessarily the most popular or the most advertised.

They’re the ones that fit your life and actually help you make better money decisions.

If you’re just starting out, try Mint or your bank’s built-in tools. They’re free and give you the basics.

If you’re ready to get serious about budgeting, YNAB is worth every penny. It’s the difference between tracking money and actually managing it.

If you just want to avoid overspending, PocketGuard keeps it simple.

The best app is the one you’ll actually use consistently. Don’t overthink it. Pick one, give it a real try, and adjust as you learn what you need.

Your money won’t manage itself, but the right app can make it a lot easier.

Remember: the app doesn’t do the work. You do. But having good tools makes the job much more manageable.

Start today. Download one app. Connect one account. Track spending for one week.

That’s how you begin taking control of your money in 2025.

People Also Ask

Which budgeting app is completely free?

Mint is completely free and always will be. Personal Capital is also free but pushes investment services. Most other “free” apps have premium versions that are much better.

Do budgeting apps actually help you save money?

Yes, but only if you use them. Studies show people who track spending reduce it by 15-20% on average. The app doesn’t save money – awareness of spending does.

Are budgeting apps safe with my bank information?

Legitimate apps use bank-level encryption and read-only access. They can see your transactions but can’t move money. Stick to well-known apps and avoid sketchy ones.

What’s the best budgeting app for beginners?

Mint for automatic tracking or PocketGuard for simplicity. YNAB is best for learning good habits but has a learning curve. Start simple and upgrade later if needed.

Can I use multiple budgeting apps at once?

Sure, but it gets confusing. I’d recommend picking one primary app for budgeting and maybe using your bank’s app for quick balance checks. Too many apps often leads to using none.

My Testing Process (So You Don’t Have To worry about)

I used each app for at least two weeks. I connected my real bank accounts, tracked real expenses, set up real budgets.

Here’s what I looked for:

- Does it sync with American banks properly?

- Is it actually free or do they trick you with fees?

- Can regular people figure it out without a tutorial?

- Does it help you spend less or just track spending?

- Do the notifications actually help or just annoy you?

Some apps looked great but crashed constantly. Others worked fine but were boring as hell.

I’m going to save you the headache and show you what’s actually worth downloading.

Read more blogs about finance on Dollar Caffeine .