My coworker thinks I’m crazy.

“You want to retire at 40? That’s impossible,” she said while buying her third Starbucks of the day.

I get it. FIRE for beginners sounds like some get-rich-quick scheme. But it’s not. It’s about living intentionally and building wealth systematically.

FIRE stands for Financial Independence, Retire Early. Thousands of people have done it. Regular folks with normal jobs who figured out how to escape the rat race decades before their peers.

I’m not talking about winning the lottery or starting the next Facebook. I’m talking about saving aggressively, investing smartly, and designing a life where work becomes optional.

This guide breaks down everything you need to know about the FIRE movement. Real strategies, actual numbers, and honest talk about what it takes to retire early.

Let’s dive in.

What the Hell is FIRE Anyway?

FIRE means Financial Independence, Retire Early. Pretty straightforward.

The basic idea: save a huge chunk of your income, invest it wisely, then live off the investment returns forever. No more bosses. No more alarm clocks. No more commuting to jobs you hate.

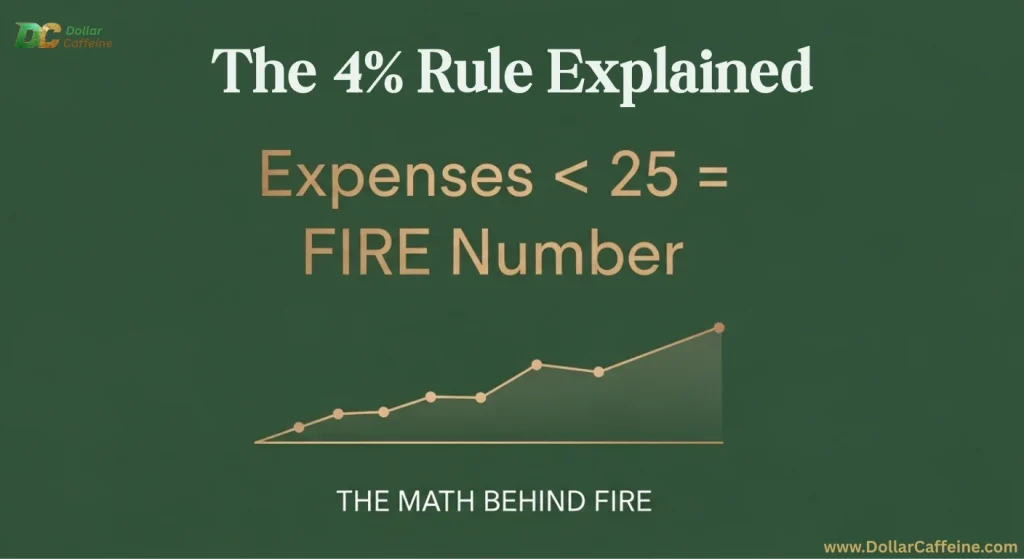

The Math Behind FIRE

Here’s the simple formula that changed my life:

Save 25 times your annual expenses. Then you can safely withdraw 4% each year without running out of money.

Example:

- You spend $40,000 per year

- You need $1 million saved ($40,000 × 25)

- You can withdraw $40,000 annually (4% of $1 million)

This is called the 4% rule. It’s based on historical stock market data and retirement research. Not perfect, but pretty damn reliable.

Why FIRE Works

Most people save 5-10% of their income and retire at 65. FIRE followers save 50-70% and retire in their 30s or 40s.

The secret isn’t making tons of money (though it helps). It’s spending way less than you earn and investing the difference.

Different Flavors of FIRE

Not everyone wants the same retirement. That’s why FIRE has different versions.

Lean FIRE

This is FIRE on a tight budget. You retire early but live pretty simply.

Target: Usually $500,000 – $750,000 Annual spending: $20,000 – $30,000 Lifestyle: Minimalist, frugal, location independent

Perfect for people who value time over stuff. You might travel to cheap countries, live in small towns, or just enjoy simple pleasures.

Fat FIRE

FIRE with all the bells and whistles. You save more but get to live comfortably in retirement.

Target: $2.5 million – $5 million+ Annual spending: $100,000 – $200,000+ Lifestyle: Travel, dining out, hobbies, nice home

This takes longer to achieve but gives you more lifestyle flexibility. You can live anywhere and do almost anything.

Barista FIRE

You reach partial financial independence but keep working part-time. Maybe for health insurance, social interaction, or extra spending money.

Target: $300,000 – $600,000 Strategy: Investments cover most expenses, part-time work covers the rest

Good for people who like their work but want more flexibility.

Coast FIRE

You save aggressively early, then let compound interest do the heavy lifting. You can switch to lower-paying jobs you actually enjoy.

Strategy: Hit a certain number by 30, then coast to traditional retirement age

This is what I’m doing. Work hard in your 20s and 30s, then relax and pursue passion projects.

How Much Money Do You Actually Need?

The standard answer is 25 times your annual expenses. But let’s get more specific.

Calculate Your FIRE Number

Step 1: Track your spending for 3-6 months

Step 2: Multiply annual expenses by 25

Step 3: Add a buffer for healthcare and emergencies

Real examples:

Sarah (Lean FIRE):

- Annual expenses: $25,000

- FIRE number: $625,000

- Timeline: 12 years saving 60% of $50,000 salary

Mike (Fat FIRE):

- Annual expenses: $80,000

- FIRE number: $2 million

- Timeline: 15 years saving 50% of $120,000 salary

The Healthcare Problem

This is the biggest challenge for early retirees in the US. Employer health insurance disappears when you quit.

Solutions:

- Move to a country with universal healthcare

- Buy individual health insurance (expensive)

- Get a part-time job with benefits (Barista FIRE)

- Use healthcare sharing ministries

Budget at least $500-1,500 monthly for healthcare if you’re going solo.

Step-by-Step FIRE Blueprint

Step 1: Get Your Financial House in Order

Before you can achieve FIRE, you need to know where you stand.

Week 1 Tasks:

- List all debts with balances and interest rates

- Calculate your net worth (assets minus debts)

- Track every dollar you spend for one month

- Set up a basic budget

Most people are shocked when they see where their money actually goes. I was spending $400 monthly on restaurants without realizing it.

Step 2: Kill High-Interest Debt

Credit card debt will murder your FIRE dreams. Those 20%+ interest rates make wealth building nearly impossible.

My debt elimination strategy:

- Pay minimums on everything

- Attack highest interest rate debt first

- Use windfalls (tax refunds, bonuses) for debt

- Consider balance transfers to 0% cards

- Don’t create new debt

Took me 18 months to clear $15,000 in credit card debt. Best financial decision I ever made.

Step 3: Build Your Emergency Fund

You need a cash cushion before aggressive investing. Emergencies will happen.

Target: 3-6 months of expenses in high-yield savings

This money sits there earning 4-5% interest. Boring but essential. When your car breaks down or you lose your job, this fund prevents you from going backwards.

Step 4: Maximize Your Savings Rate

This is where FIRE gets serious. Most people save 10%. FIRE followers save 50-70%.

How to boost your savings rate:

Housing (biggest expense):

- Get roommates or housemates

- Move to cheaper areas

- House hack (rent out rooms)

- Live in smaller spaces

Transportation:

- Buy used cars with cash

- Use public transit, bike, or walk

- Live close to work

- Skip car payments entirely

Food:

- Cook at home 80%+ of the time

- Meal prep on weekends

- Shop sales and use coupons

- Grow some of your own food

Entertainment:

- Free activities (hiking, parks, libraries)

- Potluck dinners instead of restaurants

- Streaming instead of cable

- Free community events

I went from saving 15% to 65% of my income. It took about two years to optimize everything without feeling deprived.

Step 5: Invest Like Your Future Depends On It

Savings alone won’t get you to FIRE. You need your money to grow through investing.

My simple investment strategy:

- 70% US total stock market index funds

- 20% international stock index funds

- 10% bonds or REITs

Popular low-cost funds:

- VTSAX (Vanguard Total Stock Market)

- VTIAX (Vanguard Total International)

- VBTLX (Vanguard Total Bond Market)

Expense ratios under 0.1%. Set it and forget it.

Tax-advantaged accounts first:

- 401(k) up to company match

- Max out Roth IRA ($6,500 in 2025)

- Max out 401(k) ($23,000 in 2025)

- Backdoor Roth if you make too much

- Taxable accounts for everything else

Step 6: Optimize Your Income

Cutting expenses has limits. Income growth doesn’t.

Strategies that worked for me:

At your day job:

- Ask for raises annually

- Switch companies every 2-3 years

- Learn high-value skills

- Take on extra responsibilities

- Get promoted or move to higher-paying roles

Side hustles:

- Freelancing (writing, design, coding)

- Online businesses

- Real estate investing

- Teaching or tutoring

- Selling stuff online

I doubled my income in five years through job switches and side projects. That extra money went straight to investments.

The Psychology of FIRE

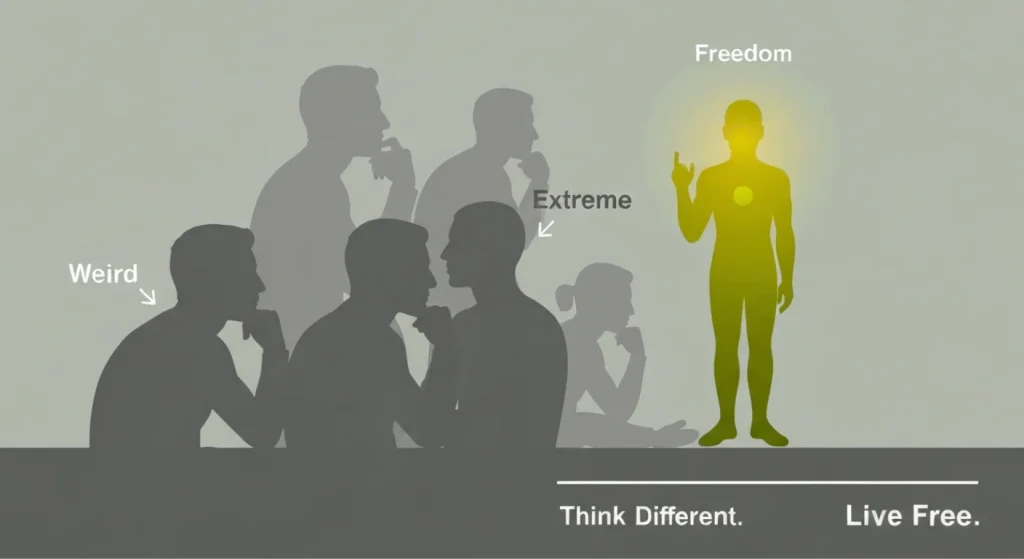

The hardest part isn’t the math. It’s dealing with other people and your own brain.

Social Pressure

Your friends will think you’re weird. Family might not understand. Coworkers will call you extreme.

How I handled it:

- Found online FIRE communities for support

- Focused on my goals, not others’ opinions

- Explained my “why” to close family and friends

- Led by example, not preaching

Lifestyle Inflation

As your income grows, spending tends to grow too. This kills FIRE progress.

Prevention strategies:

- Automate investments immediately after pay raises

- Set specific savings rate goals

- Track net worth monthly

- Remember your FIRE motivation

The Deprivation Mindset

Some people think FIRE means living like a monk. That’s bullshit.

I spend money on things I value:

- Good food (cooked at home)

- Travel (but smart travel)

- Hobbies and experiences

- Quality items that last

I don’t spend money on:

- Status symbols

- Things that don’t bring joy

- Convenience I can do myself

- Subscriptions I don’t use

It’s about intentional spending, not deprivation.

visit Reddit Financial Independence community

Common FIRE Mistakes to Avoid

Mistake 1: Not Starting

Analysis paralysis kills more FIRE dreams than market crashes. You don’t need perfect knowledge to begin.

Start with:

- Track your spending

- Open a Roth IRA

- Buy one index fund

- Increase your savings rate 5%

Perfect is the enemy of good.

Mistake 2: Extreme Frugality Burnout

Some people cut so hard they burn out and quit. Sustainable FIRE requires balance.

Cut the stuff you don’t care about. Keep spending on things that bring genuine happiness.

Mistake 3: Ignoring Healthcare Costs

Healthcare can cost $1,000+ monthly without employer insurance. Plan for this expense or it’ll destroy your FIRE math.

Mistake 4: Market Timing

Trying to time the market is a fool’s game. Invest consistently regardless of market conditions.

I kept investing through 2020’s crash, 2022’s bear market, and every dip in between. Dollar-cost averaging smooths out the volatility.

Mistake 5: Lifestyle Creep

As you get closer to FIRE, it’s tempting to relax your discipline. Stay focused until you cross the finish line.

FIRE Investment Strategies

The Three-Fund Portfolio

This is my core strategy. Simple, effective, low-maintenance.

Allocation:

- 60% US Total Stock Market

- 30% International Stocks

- 10% Bonds

Rebalance annually. That’s it.

Real Estate Investing

Some FIRE followers love real estate. It can accelerate your timeline if done right.

Strategies:

- House hacking (live in, rent out rooms)

- Buy-and-hold rental properties

- Real estate investment trusts (REITs)

- Real estate crowdfunding

Pros: Passive income, tax benefits, inflation hedge Cons: Illiquid, requires more work, location dependent

Geographic Arbitrage

Move to lower cost-of-living areas or countries to stretch your FIRE number.

Examples:

- Work remotely from small US towns

- Retire in countries like Portugal, Mexico, or Thailand

- Move from expensive cities to cheaper ones

Your $1 million goes much further in Kansas than California.

Creating Your Personal FIRE Plan

Determine Your FIRE Style

Questions to ask yourself:

- How much do I want to spend annually in retirement?

- Am I comfortable living frugally or do I want luxury?

- Do I want to work part-time or retire completely?

- Where do I want to live in retirement?

Your answers determine whether you pursue Lean, Fat, Barista, or Coast FIRE.

Set Your Timeline

Factors that affect your timeline:

- Current age and net worth

- Income level and growth potential

- Desired retirement lifestyle

- Savings rate capability

Realistic timelines:

- High earners (100k+): 10-15 years

- Average earners (50-75k): 15-20 years

- Lower earners (30-50k): 20-25 years

Track Your Progress

Monthly tasks:

- Calculate net worth

- Review spending vs. budget

- Rebalance investments if needed

- Adjust savings rate if possible

Annual tasks:

- Reassess FIRE goals

- Update investment allocations

- Review insurance needs

- Plan tax optimization strategies

Final Thoughts

FIRE for beginners isn’t about depriving yourself or getting rich quick. It’s about designing a life where money doesn’t control your decisions.

I’m not perfect at this. I still make mistakes, splurge sometimes, and question my choices. But I’m light-years ahead of where I was five years ago.

The path to financial independence looks different for everyone. Maybe you want to retire completely at 35. Maybe you want the option to work part-time at 45. Maybe you just want enough money to sleep peacefully at night.

Whatever your version of FIRE looks like, the principles are the same: spend less than you earn, invest the difference, and stay consistent for years.

Your future self will thank you for starting today. Even if you’re starting from zero, even if it feels impossible, even if your friends think you’re crazy.

The FIRE movement has given thousands of people their freedom. You can be next.

Time to get started.

People Also Ask (Advanced FAQ)

Can you really retire at 40 with FIRE?

Absolutely. Thousands of people have done it. The key is saving 50-70% of your income and investing consistently. It requires discipline but it’s completely achievable.

How much do I need to retire early?

Use the 25x rule: multiply your annual expenses by 25. If you spend $40,000 yearly, you need $1 million. Lean FIRE might need $500,000-750,000 while Fat FIRE requires $2 million+.

Is FIRE realistic for average income earners?

Yes, but it takes longer. A teacher making $50,000 can achieve FIRE, but might need 15-20 years instead of 10. Higher savings rates and side income help accelerate the timeline.

What if the stock market crashes after I retire?

This is called sequence of returns risk. Have 1-2 years of expenses in cash. Consider working part-time during market downturns. Historical data shows markets recover over time.

Can I do FIRE with kids?

It’s harder but possible. Kids cost money, but many FIRE families make it work through careful budgeting, geographic arbitrage, and creative lifestyle choices.

What’s the biggest FIRE risk?

Running out of money due to higher-than-expected expenses, healthcare costs, or poor market returns. Build buffers and consider part-time work as backup.

How do I handle healthcare without employer insurance?

Budget $500-1,500 monthly for individual insurance. Consider states with better ACA plans, healthcare sharing ministries, or moving to countries with universal healthcare.

Should I pay off my mortgage before FIRE?

Depends on interest rates and your risk tolerance. If your mortgage is 3%, investing might give better returns. If it’s 6%+, consider paying it off for guaranteed returns.

Read more blogs about Finance on Dollar Caffeine